Cashflow, debt, and the CEB’s financial future

Cashflow, debt, and the CEB’s financial future

W(h)ither the power supply of Sri Lanka?

Disclaimer -

Sri Lanka’s energy sector is an absolute mess.

We know this intuitively of course, what with the massive powercuts and fuel queues we had in 2022. But the extent of the absolutely ridiculous chaos that is present within the sector is just too mindboggling. I’ve been trying to write about this since August, and keep coming up with more and more complicated and worrying data. There is the question of decades of mismanagement, lack of planning, and of course outright corruption and even graft in the system.

For this piece, I’m not writing of any of that, but rather focusing on the current financials and financing the future. This doesn’t mean that all these problems aren’t true and real, and implementing any of what I’m talking about won’t run into the same challenges as in the past. Addressing those points will still remain critical to moving forward in anyway.

As part of how I’m writing this piece, I’m giving a series of numbers and assumptions. Note that these numbers aren’t meant to be exact, they are estimates and approximations only - the actual numbers very likely differ from these in some ways. But on an overall basis these numbers should be close enough to the real numbers to get a sense of the magnitude of the problem, and the magnitude of how the problem has to be solved.

Tariffs rising again and a possible coal shortage is bringing to mind some of the worst points of 2022 - long powercuts, long fuel queues, and an absolute desperation in the people. Moving into 2023, this type of news is really not what we want - especially given the relative improvement in operational activities since the middle of 2022. Can we make sense of this? Could we have avoided it?

Sri Lanka’s energy sector is truly a pathetic animal. Plagued by years of losses, decades of mismanagement across the board, and just no consistent plan (or implementation of existing plans), it’s been basically crawling along for the last few months. But given how critical it is, it’s something we need to keep alive and save, even if it’s painful. In this piece, I’m not going into the history of the energy sector, or exploring what went wrong - instead, I’m going to focus on some very specific, yet absolutely critical parts of the whole puzzle - CEB’s cashflow problems, a bit on accumulated debt, and what these 2 points mean for the energy sector financials of Sri Lanka.

CEB’s cashflow problems - Massive rise in costs, revenue never keeping up

Global energy price boom and LKR depreciation driving up raw material costs

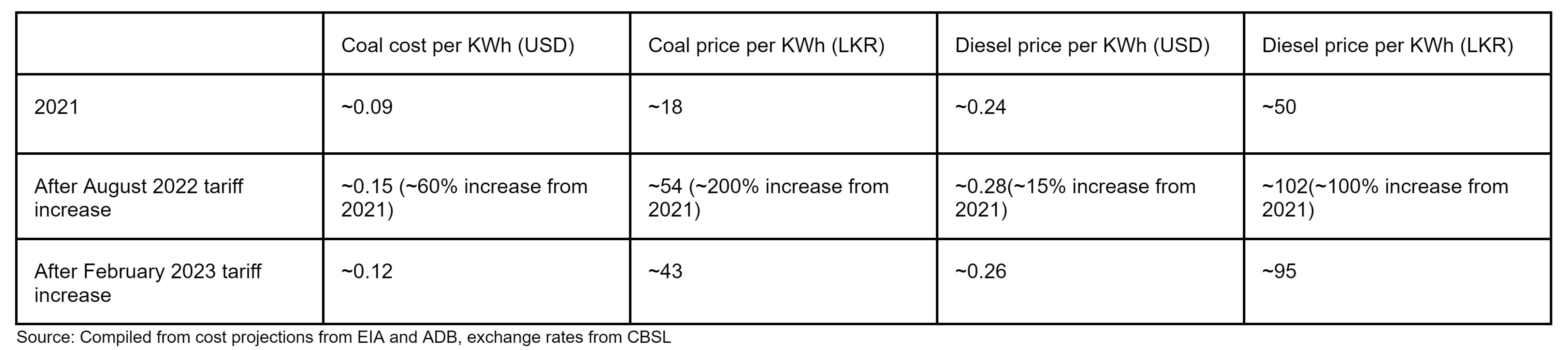

From end-2021 to end-2022, Sri Lanka’s energy costs have skyrocketed, primarily driven by the rise in global energy prices adding on top of the depreciation of the local currency (given that the exchange rate worsened by 80%, a big chunk of the price increase is on this basis). The following table shows an approximate illustration of how these costs have moved from 2021 until the most recent tariff increase. These numbers are taken from varied global sources for the global price of coal and diesel in USD terms for energy generation, and adjusted for the existing exchange rate at the time.

In reality, actual prices for individual countries would vary from these numbers - but this should serve as a base for understanding the major cost drivers. The diesel price applicable for Sri Lanka could be slightly higher than these numbers given the premium that petroleum suppliers seem to have placed on supplying to Sri Lanka given the credit risk, while coal prices might be slightly lower (though given that Sri Lanka’s coal suppliers are charging Sri Lanka on a blended price index, this might not be much lower).

Generation costs and raw material costs count for far more than personnel and administrative costs

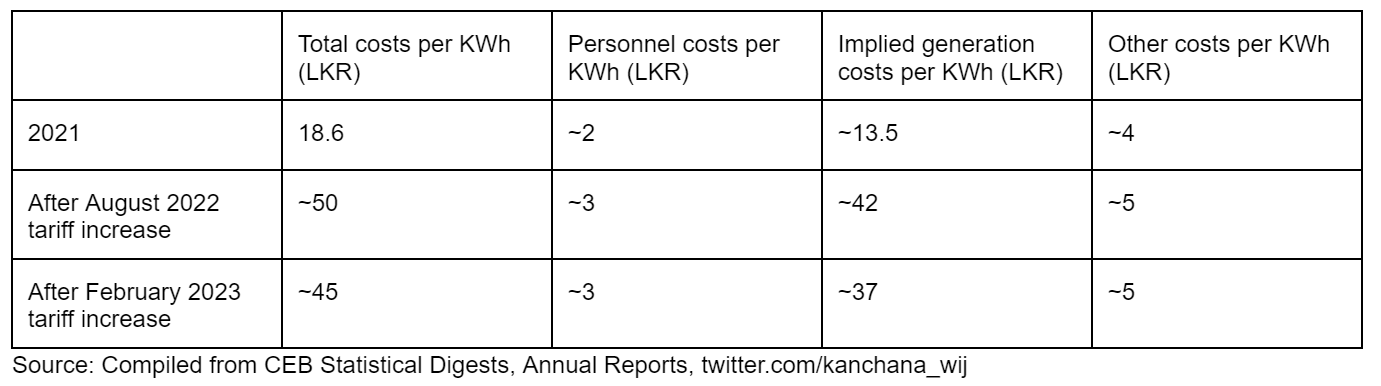

While the direct raw material costs have gone up a lot, it’s also likely that other costs have gone up as well. A major claim locally, is on the high personnel costs in the CEB as well. Beyond these, there are also administrative costs that likely apply. While we don’t have direct information for what these currently look like, we can get a sense of what this could be by looking at some overall cost numbers and personnel cost numbers implied by some information that was released by the Minister of Power and Energy, along with the implied generation costs.

Do note that there is somewhat of an accounting treatment here - I’ve included depreciation costs and material costs in the implied generation costs, and accounted for financing costs in other costs. The total costs for August and February are also approximate values, and the real values could be in a range around what I’ve mentioned. That likely accounts for why the “other costs” stay the same in this exercise” despite realistically it makes sense they would have risen. (EDIT: I had made a mistake and put some aggregate values instead for other costs. In reality, the other costs per KWh have risen (as have personnel costs) since the total spending on those categories hasn’t shifted too much, while the number of KWh have fallen. Thanks to the reader who pointed this out)

What this data shows, is that despite the personnel costs being quite large in absolute terms (around 3-3.5 bn LKR per month!), they’re only a relatively small component in context of the overall costs of the CEB, which are primarily driven by costs related to generation (between 70-90% depending on what is included within this category). That makes it clear that the primary cost issue that the CEB is facing has more to do with direct generation costs rather than high administrative costs.

The CEB’s cashflow is likely around neutral on average after February 2023 - and positive in months with more hydro

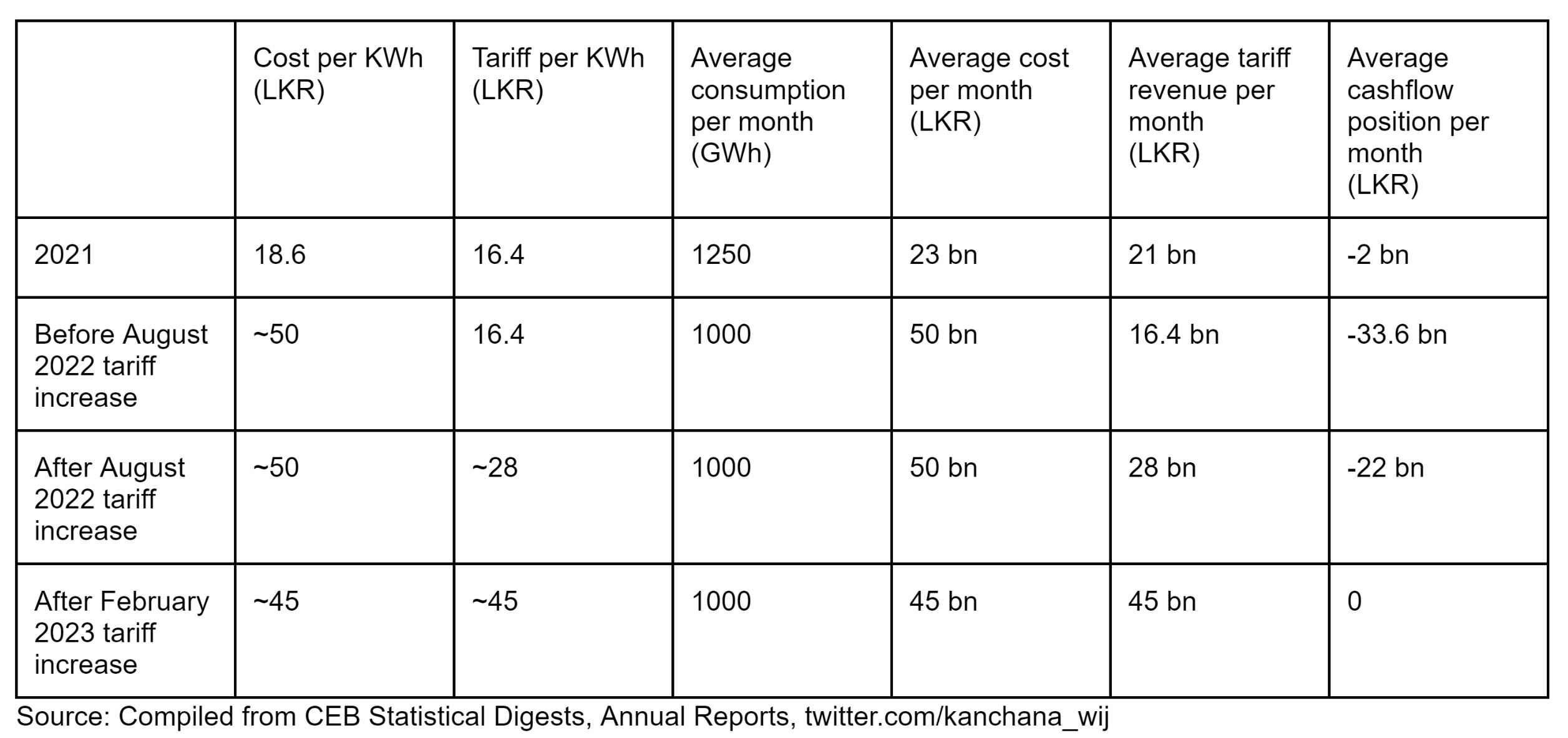

Tabulating all this information together with consumption numbers results in a prediction for what the overall cashflow of the CEB would have looked like in 2021, before the August tariff rise, after the August tariff rise, and after the February tariff rise.

What this implies is that even with costs falling a bit from August to February, the fact that revenue was still highly negative was a problem. The CEB had negative cashflow, around 10 times as bad as it did in 2021, even after the August tariff increase (Before the tariff increase, this was even higher - with cash flow being more than 15 times more negative than in the past). The most recent tariff increase likely turns to cashflow neutral, and possibly positive in certain months as well (mostly in months with more hydroppower generation).

Cashflow is likely bunched up in some months - meaning far more stress right now

However, it’s also not necessarily true that these average negative cashflow numbers I refer to are spread across the year. In reality, given a big chunk of these would be trade related payments, most of the costs would in fact, be bunched up. An example of this is what the reported numbers for the coal payments for the 1st quarter of 2023 are likely to be. There seems to be about LKR 50 bn in payments needed to get a coal shipment for the April to September 2023 period, as well as a further LKR 50 bn on payments for shipments advanced for January and February. Coal alone seems to account for a cashflow requirement of LKR 100 bn in the 1st quarter of 2023 alone - petroleum costs as well as financing costs likely account for a significant amount more. I think it looks clear that the CEB simply did not have the cashflow to make payments of such a magnitude.

As long as the CEB was in a negative cashflow position, especially given it would have been a significantly worse position than in the past, meeting these requirements would have been barely possible. In the context that the CEB was not able to make the LKR payments needed to purchase the USD for coal imports, it’s quite likely that the coal supply would have been hindered. This would have been similarly true for other petroleum payments, and there was some allusion made to this point as well in local media. The CEB, despite being a monopoly provider of energy, could simply have been forced into massive blackouts again, simply on a cashflow basis.

The debt of the past - a legacy that couldn’t be continued

Now if any firm had been running on a negative cashflow (and doing so for most years in the last decade), the only way that this would have been possible is if there was something that bridged that negative cashflow. In CEB’s case, this was a combination of transfers from the treasury and credit from banks, primarily the state banks - Bank of Ceylon and People’s Bank.

The most up-to-date financial information we have on the CEB is from end-September 2022, from the CEB’s disclosures to the CSE due to its listed debenture. Here, the data shows that at end-September 2022, the CEB had approximately LKR 360 bn (around USD 1 bn) in current liabilities, as well as a further LKR 540 bn (almost USD 1.5 bn) in non-current liabilities. It is likely that further debt was accumulated from September to February as well, given the CEB was in a negative cashflow position here as well.

Now how is the CEB going to meet these payments moving forward? In the short term, given the CEB IS the monopoly provider of electricity for Sri Lanka, the new tariff regime implies a future where the cashflow problems are handled. While the actual cashflow would take some time to come in, this future projection is likely strong enough for the state banks to provide some extra credit to the CEB to survive until the cashflow comes in. This is how the CEB is able to “guarantee” full power after the tariff increases - access to credit to purchase generation fuel. After this, however, the problem still remains. There might not be too much extra cashflow left in case energy costs don’t fall a lot - which means the probem might merely be pushed into the future instead. This is especially worrying for the financials of the state banks themselves, as such large amounts of debt being taken on by them, with low chance of repayment, has significant financial sector risks as well.

The future financials of Sri Lanka’s energy sector - Move fast or the moment may be past

These financial costs, which are in effect, largely the costs of providing subsidised electricity in the past, remain a key challenge. Given the role that depreciation plays in the costs of the CEB, even if global costs fall, any future depreciation could offset at least part of this fall, further limiting the space to meet past liabilities. All of this means that for a government that might have an admirable reason to advance electrification in the country, especially among low-income consumers, the space to do this becomes very limited.

To be very clear, I think the fact that the current tariff increases are disproportionately at these lower income levels is in itself a terrible thing. However, I also don’t see too much of a way around that - raising tariffs too much on the higher income categories likely means moving them out of the grid altogether, reducing the extra revenue the CEB could get anyway. In a future article, I’ll explore what could have been done and what could be done even now to move towards a more equitable result for those who have drawn the short-end of the stick.

In any case, the built up liabilities of past subsidies, past finance costs, and past payments is a reality that the CEB has to reckon with. Moving to improve the current cashflows in itself, becomes a hard option right now - since the immediate installation costs of low-cost renewable sources would once again push the CEB into negative cashflow territory. These facts are probably part of the reason why the CEB’s restructuring hasn’t moved forward as fast as we would have liked, and why simple privatization is not necessarily an easy option - who would want to buy such an organization? The tariff increases should make it easier to move ahead with the process given the CEB is likely not cashflow negative anymore, but the accumulated debt remains.

Here, I believe 2 overall solutions can be part of the future. First, would be to explore direct concessional financing for the development of low cost energy generation. The Asian Development Bank in particular, could be a critical stakeholder here, especially given that even private investment could work within the structure of the ADB through a blended financing arrangement for Sri Lanka’s energy sector. Second, would be to ringfence the current liabilities separately from the current structure, and possibly explore moving these liabilities to the state treasury directly (given that in practice, the CEB might not be able to pay these off anyway, meaning the treasury might anyway have to step in). This could help make the current existing CEB a lot “cleaner” in it’s financials, and much easier for any investment and restructuring to happen. Again, financing from the multilaterals can be part of what protects from the financial sector risks stemming from the energy sector’s existing debt.

Sri Lanka’s energy sector problems aren’t of course, limited to the CEB, but the CEB’s role as the country’s electrifier means dealing with these problems are absolutely critical. In the end, the future pathway of Sri Lanka will very likely be tied to how well these problems are resolved - if the energy sector remains in crisis, that could very well be both a growth and a debt issue that lasts for a while. Even the multilateral financing needed for both the direct problems in the energy sector and the knock-on financial risks could mean that the multilateral’s financing ability for the rest of the economy could be limited as well.

On the other hand, resolving these issues will likely mean a much more robust Sri Lanka, and one where one of the most fragile debt-generators in the economy no longer remains able to create the same problems as in the past. Recognizing the pivotal role that the energy sector has played in the Sri Lankan debt story, addressing this could end up being far more critical for macroeconomic stability than it may seem on the face of it.

The situation is at a critical stage where inaction can easily result in a spiralling situation in the past. But the fact that things are so fragile, is in itself, a moment for hope. There is simply no option but to fix this hole, the costs are too high, will accumulate too soon, and will be too widespread if not addressed. On that basis, I think there is enough being done now (though again, a lot more clarity and trust can be built in the process) that implies that things are moving in the right direction. If we stick to that, the country’s future could be a little brighter (we’ll have more lights on after all!). Let’s hope Sri Lanka goes down this path and avoids the mistakes of the past.